During periods of monetary tightening, rebalancing of domestic demand is expected to positively affect the foreign trade balance and the current account balance. [1] The latest monetary tightening cycle, which began in June 2023 and gradually raised the policy rate from 8.5% to 50% by April 2024, affects various macroeconomic indicators besides inflation, including foreign trade and the current account balance. In this blog post, we provide a descriptive analysis of the effects of the recent monetary tightening on Türkiye’s foreign trade and current account balance. To do so, we assess the current developments and present our short-term projections while also zooming in on the two previous major episodes of monetary tightening in recent years.

In our analysis, we define the tightening periods based on the interval between the lowest and highest values of the one-week repo rate within the related episode. Accordingly, the first reference period of tightening corresponds to the one-year period between the third quarter of 2018 and the second quarter of 2019. During this period, the policy rate surged to 24% in September 2018, up from 8% in May 2018, and remained steady at this level until July 2019. The second tightening period spans one year, starting in the last quarter of 2020 and ending in the third quarter of 2021. This period saw a gradual increase in the policy rate, which went from 8.25% in August 2020 to 19% in March 2021 and stayed at this level until September 2021.

While the total increase in the policy rate during the tightening period starting in 2018 was 1,600 basis points, it was 1,075 basis points in the period starting in 2020. As for the current period, the policy rate has increased by a total of 4,150 basis points since June 2023.

The specified tightening periods are shaded in the charts throughout this blog post for ease of visualization.

Foreign Trade Developments and Real Rebalancing

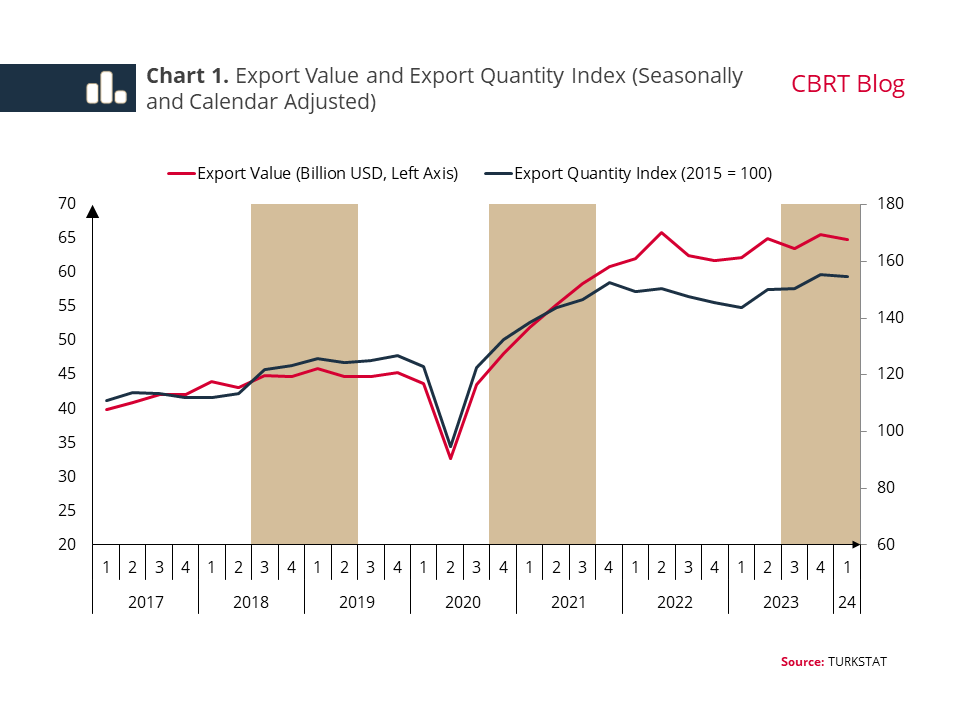

A glance at the development of exports reveals that during the first tightening period, exports remained stable in nominal terms and increased moderately in real terms (Chart 1). In the tightening period starting in 2020, it is clearly seen that both nominal and real exports recorded strong increases owing to the post-pandemic recovery in international trade.

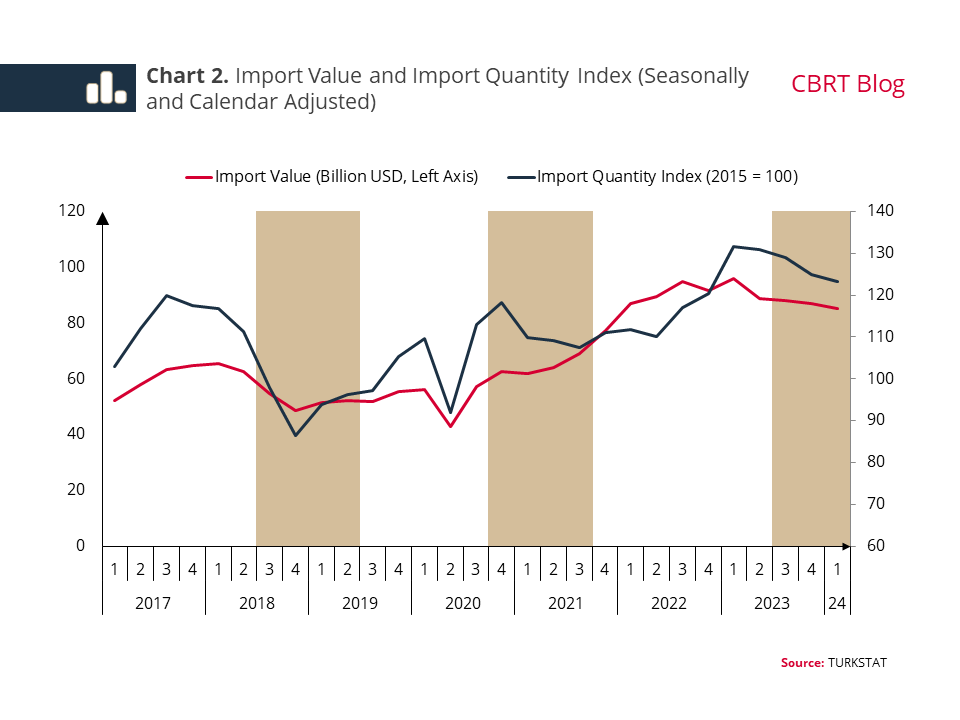

An analysis of these periods in terms of imports indicates that imports first declined significantly and rapidly in both nominal and real terms during the first reference tightening period that started in 2018, then recovered but remained below the pre-tightening level for a long time (Chart 2). However, we do not observe the expected decline in imports from the nominal import data during the second reference period of tightening. On the other hand, USD-denominated import prices increased by 24.2% in 2021 year-on-year, also driven by the post-pandemic recovery in global demand. Accordingly, imports are observed to have decreased in real terms during the same period. This fact underscores the significance of interpreting the impact of monetary policy on import demand in real terms.

Turning to the current tightening period, exports remain robust in nominal terms, backed by external demand, with a mild uptrend in terms of quantity (Chart 1). On the import front, with the effects of monetary tightening on demand, nominal and real imports have declined markedly since the second half of 2023 through the first quarter of 2024 (Chart 2).

In short, we see that in the current tightening period, exports continue to increase, while imports are decreasing in line with the tightening in monetary and financial conditions, as was the case in the previous tightening periods. These observations indicate that, similar to previous periods, monetary tightening has prompted a real rebalancing in foreign trade.

Current Account Balance and Sub-Items

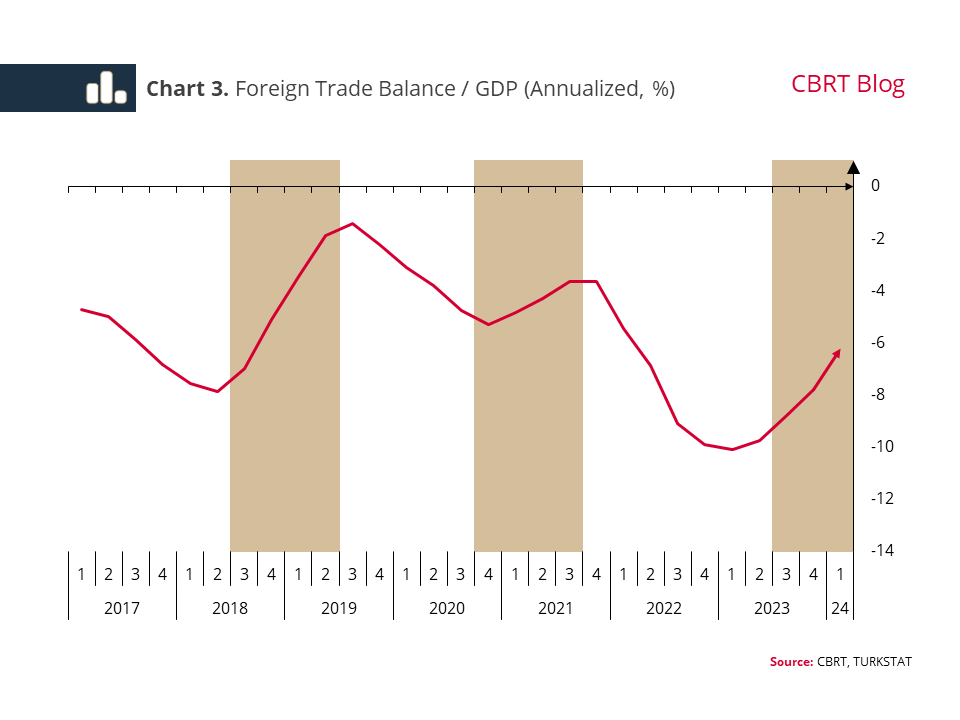

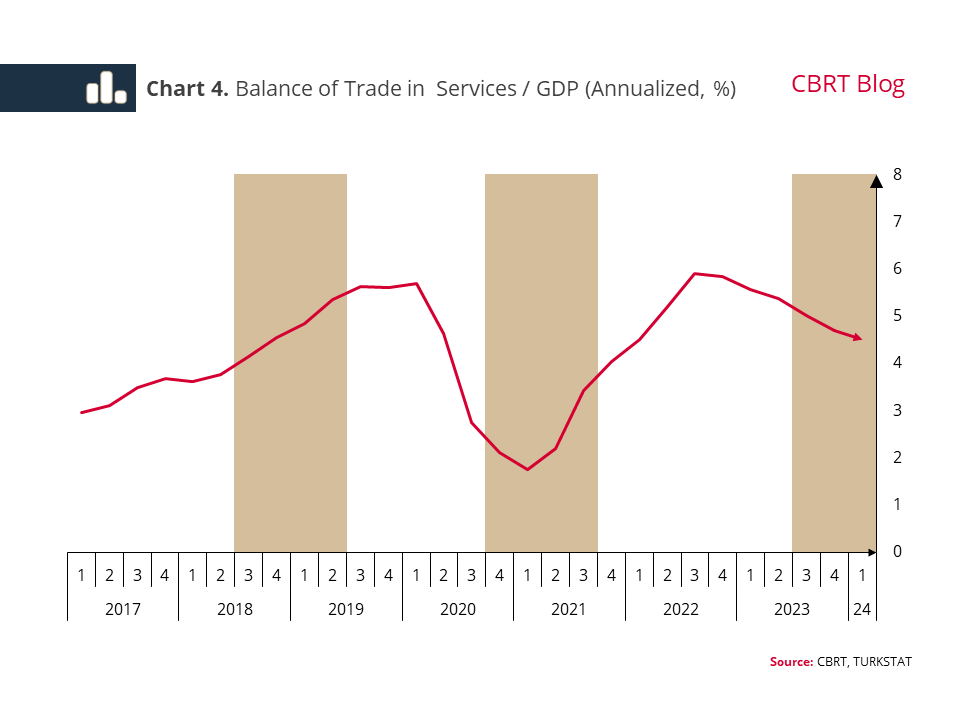

In this context, data reveal that the foreign trade balance as a share of GDP registered a significant improvement during the relevant tightening periods (Chart 3). As the foreign trade balance accounts for an important share of the current account balance, such a solid improvement in the former during monetary tightening periods is reflected in the latter. On the other hand, trade in services, another important subcomponent of the current account balance, is also a determining factor for the degree of the improvement in the current account balance in such periods. During our two reference periods of monetary tightening, when domestic demand was subdued, the tourism revenues-driven services balance significantly contributed to the improvement in the current account balance. However, in the second half of 2023 covering the latest tightening period, the services balance as a share of GDP declined somewhat, albeit still remaining strong (Chart 4).

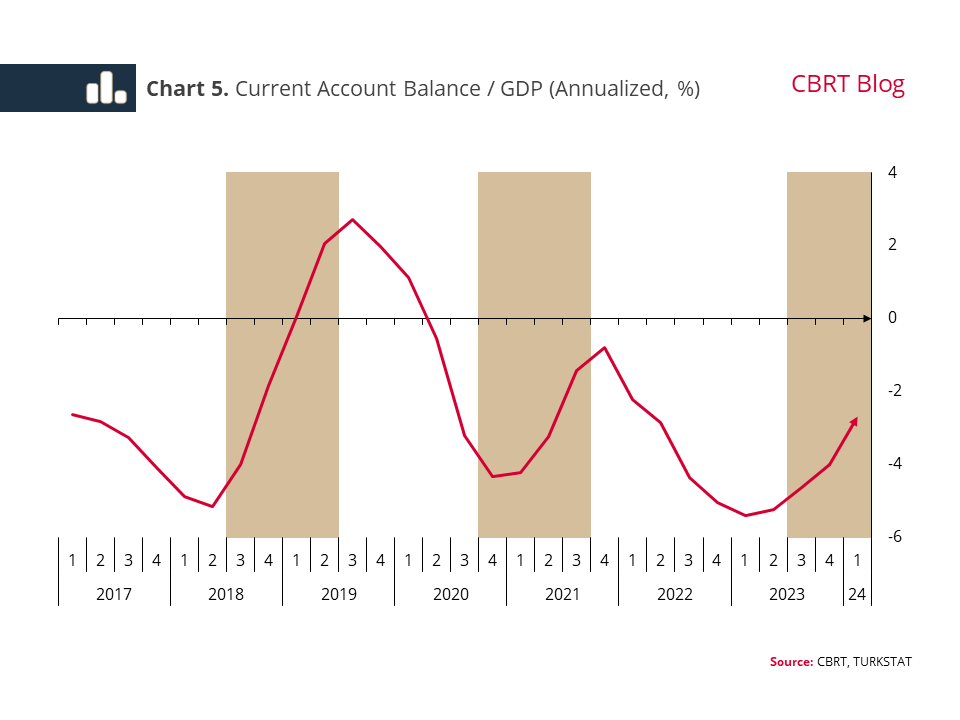

When we look at the overall course of the current account balance led by these two sub-items of trade, we see significant improvements in both reference periods of tightening (Chart 5). During the first period starting in 2018, the current account balance improved sharply, closing the deficit and even running a surplus. A similar recovery was also observed during the monetary tightening period that started in 2020. In this period, the ratio of the current account deficit to GDP decreased considerably on the back of the real rebalancing in foreign trade and the improvement in the services balance despite large increases in import prices in 2021.

Regarding the ongoing monetary tightening, despite the decline in the ratio of the services balance to GDP, the current account balance trend has recorded a significant improvement. This improvement was backed by the real rebalancing in the goods trade that started in the second half of 2023 and continued through the first quarter of 2024, as implied by the quantity indices. Current data indicate that the improvement continued in the first quarter of the year and the current account deficit to GDP ratio receded to 2.7%. In the second half of 2024, as the lagged effects of monetary transmission kick in, we project a further improvement in the current account balance along with a more evident rebalancing in domestic demand. We estimate that the potentially adverse impact of the expected appreciation in the real exchange rate on the current account balance will be more than offset by the rebalancing in domestic demand. [2]

[1] Theoretically, relative price changes are also expected to affect the foreign trade balance, but in this blog post, we adopt a narrative based on domestic demand, which has a larger impact on the external balance. For the effects of income and relative price variables on imports, see Çulha, Eren and Öğünç (2019) and Iossifov and Fei (2019).

[2] Studies in the related literature report that the effect of the real exchange rate on exports is limited and exports are mainly driven by external demand (Çelgin, Gökcü and Özel, 2019; Kazdal and Gül, 2021; Demir, Kazdal and Gül, 2023).